Case Details: Kanam Latex (P) Ltd. Versus Commissioner of GST & Central Excise, Tirunelveli (2025) 32 Centax 321 (Tri.-Mad)

Judiciary and Counsel Details

-

S/Shri P. Dinesha, Member (J) and M. Ajit Kumar, Member (T)

- Shri Hari Radhakrishnan, Adv., for the Appellant.

- Shri Anoop Singh, JC, Authorized Representative, for the Respondent.

Facts of the Case

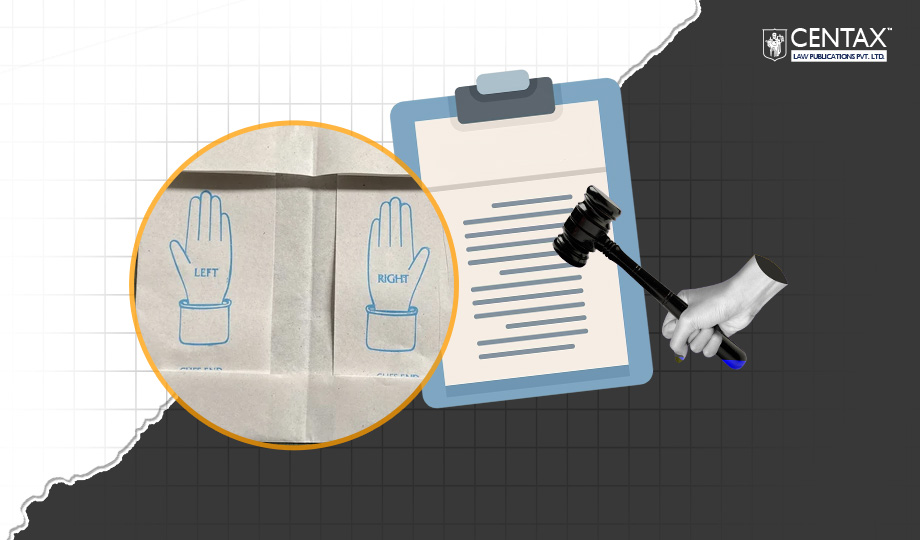

The appellant, a manufacturer and supplier of packaging materials for surgical and examination gloves, argued that their product, known in trade as ‘surgical glove inner wrap/wallet’, should be classified under Tariff Entry 4817 30 90 of the Central Excise Tariff Act, 1985, as paper wallets. This product was made by processing special reel-form paper through printing, cutting, and folding, creating a three-sided open printed paper wrap. This wrap was used to encase a pair of surgical gloves before placing them in a larger retail box. The appellant claimed these items functioned as ‘wallets’ in commercial use and supported this by referencing dictionary definitions. The adjudicating authority, however, classified the goods under Tariff Entry 4823 90 13 as packing and wrapping paper. The case was then placed before the CESTAT Madras.

CESTAT Held

The CESTAT held that no service tax could be levied on notional interest earned on security deposits received from service recipients. Referring to precedents, the Tribunal concluded that such notional income does not fall within the value of taxable service under section 67 of the Finance Act, 1994. The impugned order was set aside.

List of Cases Cited

- Amazon Wholesale India Pvt. Ltd. v. Customs Authority of Advance Ruling — (2023) 13 Centax 219 (Del.) — Relied on [Para 6]

- Commissioner v. Maa Printers — 2017 (8) TMI 776-CESTAT Bangalore — Referred [Para 3.2]

- Pyarali K. Tejani v. Mahadeo Ramchandra Dange — [1973] INSC 196 — Relied on [Para 8]

- Shuban Prints v. Commissioner — 2019 (366) E.L.T. 756 (Tribunal) — Referred [Para 3.2]

- Smash Colour Prints and Packaging Pvt. Ltd. v. Commissioner — 2015 (7) TMI 583 — Referred [Para 3.2]

- Uniworth Textiles Ltd. v. Commissioner — 2013 (288) E.L.T. 161 (S.C.) — Referred [Para 3.1]